Looking ahead this year, the automotive job market appears weak but stable, while inflation is expected to decline, according to a 2024 Cox Automotive Industry Insights Webcast report for the United States.

The report also highlights that consumer sentiment has increased and is improving (though, while spending has also increased, growth is actually slowing), and that interest rates are still high (but are on the decline).

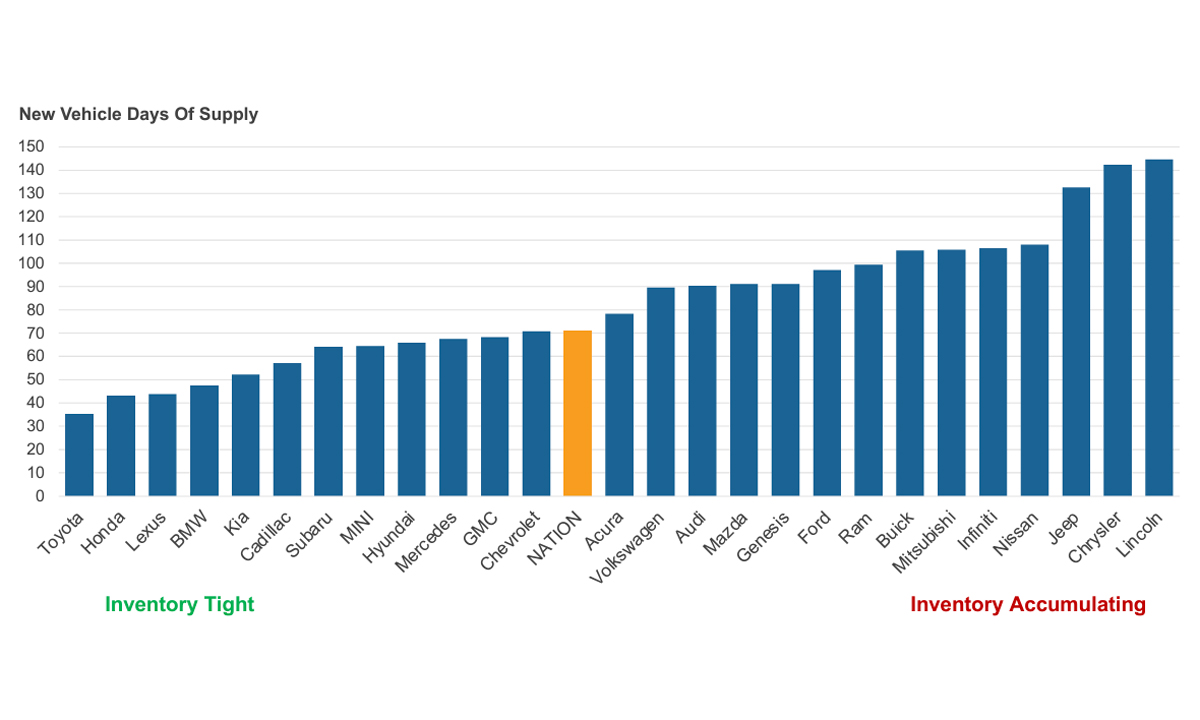

A bumpy recovery is expected for new vehicle sales this year, which finished 2023 with 15.46 million units. The good news is that new vehicle inventory finished the year up 51% compared to 2022 — although the situation around brand inventory remains varied as some brands are still limited in availability. Beyond new vehicles, pent-up rental and commercial demand is being unleashed, though continued growth will be difficult.

Electric vehicle sales were up in the last quarter of 2023, but only slightly from Q3, while a year-over-year growth of 46% in 2023 helped push total sales to 1.1 million. However EV adoption remains uneven across the nation and the share of EV retail sales represents only 7.4% — and that’s nationally. California has the greatest share of EV retail sales at 21.1 %, followed by Washington with 15.4%, New Jersey with 10.3%, then you have the nation overall at 7.4%, followed by other states that fall increasingly below that percentage.

And yet, EV inventory is well above the industry average having increased by 92% last year. EV inventory averaged 113 days’ supply to end the year. Also worth noting is that EV prices are near parity with ICE vehicles thanks to a surplus in inventory, higher incentives, and competition. And perhaps as a result of this and/or a number of other factors, EV leasing is expected to rise this year, with stricter eligibility for IRA tax credits.